1Q26 earnings: Antero's transition to dry gas

Which pipeline capacity will it let go, and which companies could it buy to backfill its FT?

This is the second in a series digging into the most interesting topics from 1Q26 earnings season. Last week, I covered midstream operators’ commentary on Permian production growth relative to takeaway capacity additions.

Antero’s late-2025 transactions — divesting its Utica position and acquiring HG Energy — marked a substantial shift in the company’s strategy. Following those deals, Antero is much more weighted toward dry-gas volumes, and the company’s 1Q26 commentary reinforced the shift, highlighting its interest in additional West Virginia acquisitions and signaling that it won’t renew some processing and firm transmission agreements.

For Antero, dropping FT implicitly acknowledges that its West Virginia rich-gas production won’t grow into the FT portfolio designed for it. Antero is not alone among Appalachian operators in having a limited inventory runway on its core assets. But the more it can bulk up by acquiring other companies whose assets it can integrate into its midstream positions, the less it needs to right-size its FT portfolio. Key FT renewal decisions next year will reveal what Antero’s management thinks of its potential to be a West Virginia consolidator rather than an acquisition target itself.

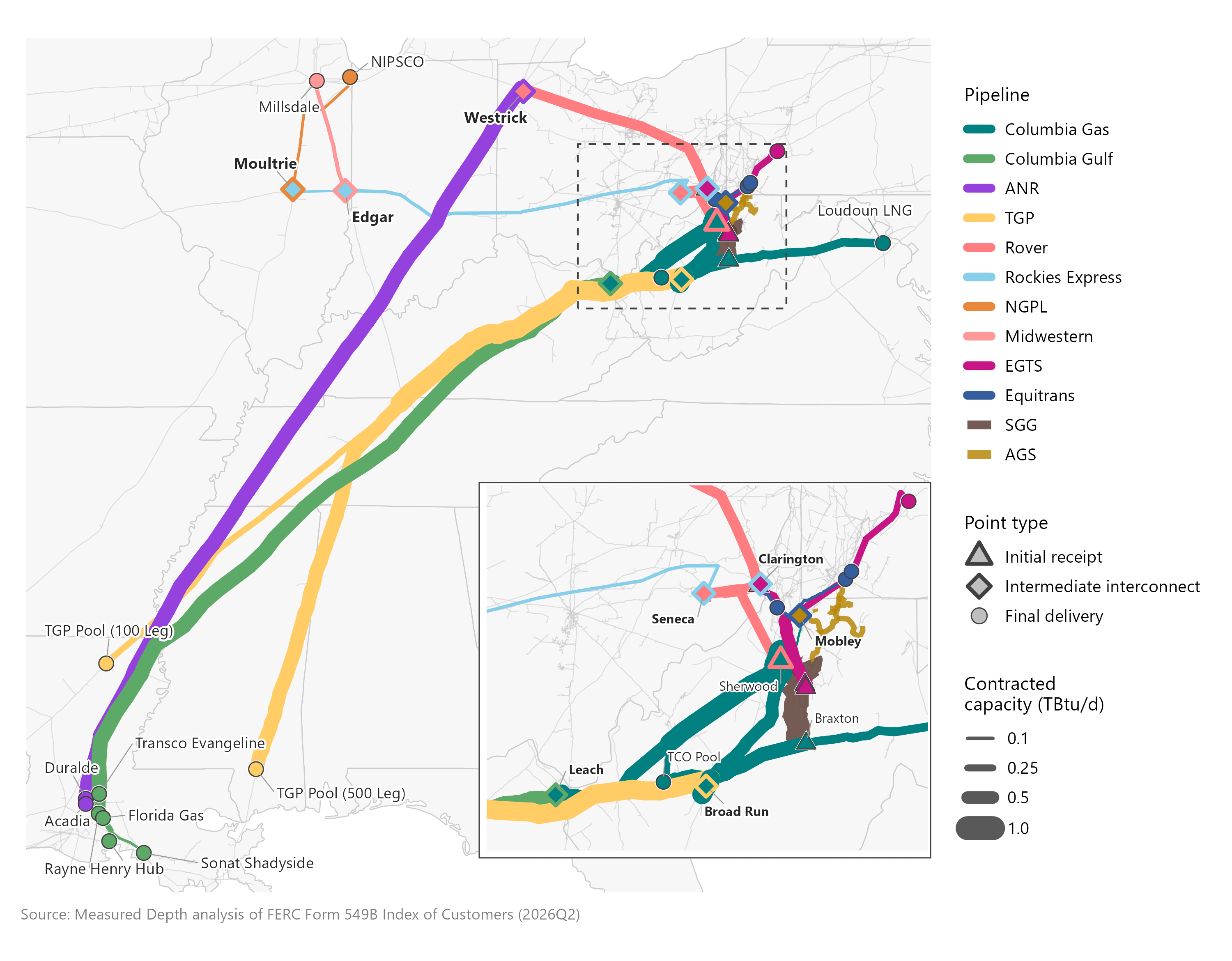

Antero’s capacity position post-HG

Historically, Antero distinguished itself among Appalachian peers by contracting early for pipeline capracity to move gas out of the basin. The challenge with Antero’s portfolio, though, has always been that it is bespoke to Antero and overwhelmingly originates at MPLX’s Sherwood/Smithburg gas processing plant complex, which processes little non-Antero gas. Antero’s in-the-money capacity, therefore, cannot be monetized independently of its own production. Conversely, if, say, CNX’s Marcellus production were to decline, the company could buy another operator’s gas in-path and still capture the value of its in-the-money pipeline capacity.

With its acquisition of HG and divestiture of its Utica properties, Antero’s FT portfolio underwent two key changes:

Antero inherited HG’s portfolio, which consists entirely of in-basin FT, moving HG’s gas from southern West Virginia into liquid markets on EGTS, Columbia Gas, REX, and TETCO.

Infinity took on 300 BBtu/d of Antero’s 400 BBtu/d of REX capacity. Antero can likely use the remaining REX capacity1 to improve realized prices for some HG production that previously was delivered into REX.

Figure 1 | Pro-forma Antero FT portfolio

Between redeploying its REX capacity to improve market access for HG volumes and HG’s capacity on DT Midstream’s systems that Antero also uses, HG’s midstream position fits well with Antero’s.

Which FT is Antero likely to drop?

Keep reading with a 7-day free trial

Subscribe to Measured Depth to keep reading this post and get 7 days of free access to the full post archives.