1Q26 earnings: Midstream operators don't expect Permian takeaway capacity to fill

So why is the market suddenly so bullish on Permian gas growth?

Last quarter, I wrote a “five most interesting things” wrap-up of earnings season, but 1Q26 earnings season raised bigger questions that I thought warranted more comprehensive treatment. This post, looking at Permian production versus takeaway capacity, is the first in that series.

The biggest questions weighing on the gas market right now concern Permian gas production: how much is currently curtailed and how much production will grow once new pipeline capacity is online. As always, the challenge with forecasting Permian gas production is that we don’t have a solid starting point: regional dry-gas production is never reported, complete wellhead gas production isn’t reported to the Texas Railroad Commission for a year or more, and pipeline scrapes capture less than half of the region’s volumes.

With no good way to bridge these gaps, the market is clinging to the signals it has: rising gas-oil ratios, negative Waha prices since early February, two new gas processing plants announced this quarter. Midstream operators probably have the best basin-wide view, since they work with multiple producer counterparties. But the lack of a common starting point makes their comments hard to interpret, and the market misread many of them. A more careful analysis reveals Enterprise, Energy Transfer, Summit, and Targa all expect Permian gas production will not fill the ~11 Bcfd of takeaway capacity under construction.

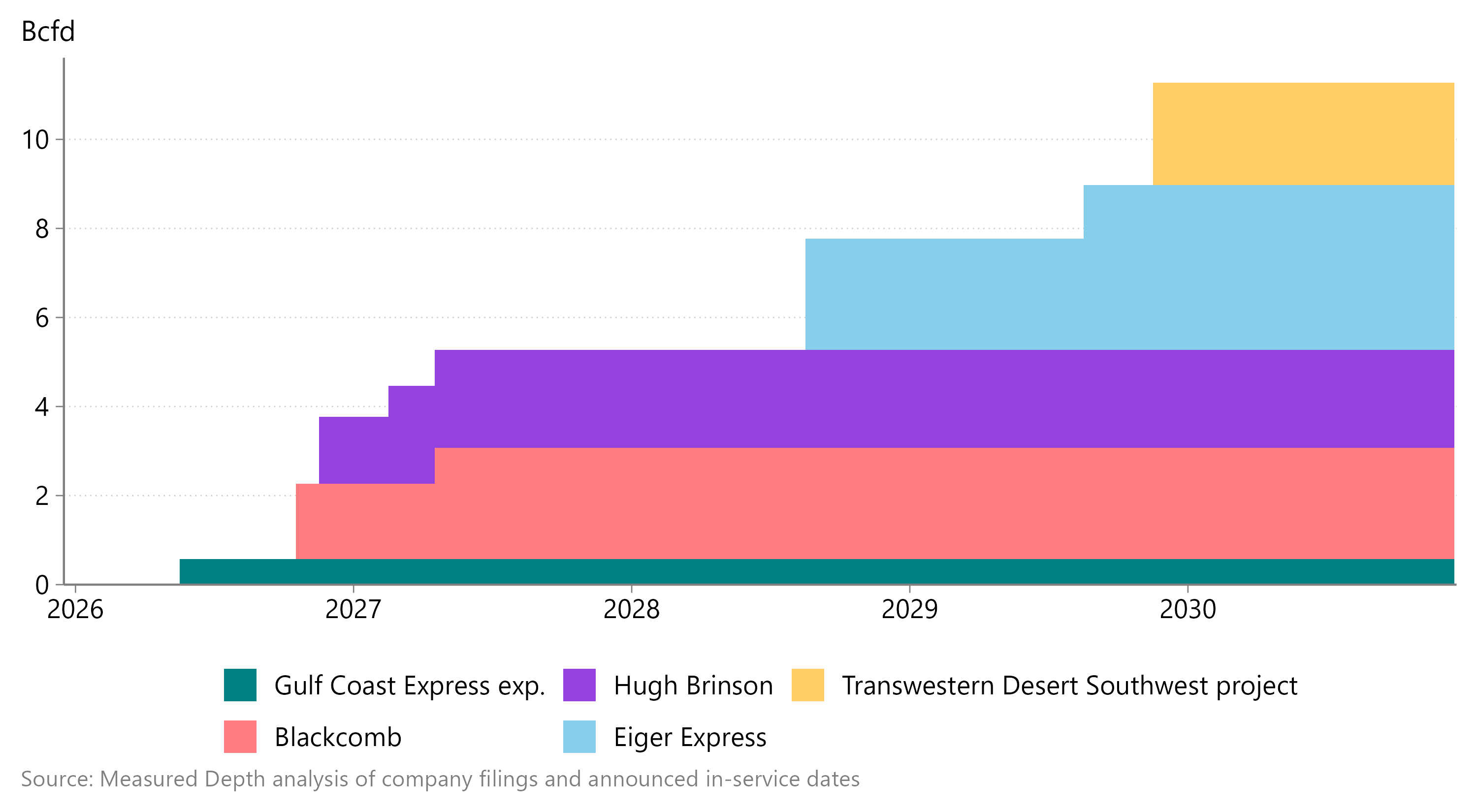

Figure 1 | Post-FID Permian takeaway capacity

Energy Transfer’s refutation of the processing-additions school of Permian production forecasting

Energy Transfer was unequivocal: Permian gas production growth won’t match the pace of takeaway capacity expansion:

Could you say there’s a bottleneck in the Permian Basin today? Absolutely. By the … first part of next year, that bottleneck is going to open up, and there's going to be enormous opportunities for producers to drill away as much as they want to drill because there’ll be plenty of capacity for a number of years to come.

Just as importantly, Energy Transfer refuted what I’ll call the processing-additions school of Permian gas production forecasting. The processing-additions school holds that, without current well data or comprehensive pipeline scrapes, scheduled processing-plant additions are the best way to forecast gas production growth. And there’s merit to this approach, since midstream operators typically don’t build new processing capacity without commitments from producers.

But it has its pitfalls, too: some commitments to new capacity may just replace expiring contracts on older capacity, and Energy Transfer pointed out1 that some midstream operators are more aggressive with their growth plans:

Keep reading with a 7-day free trial

Subscribe to Measured Depth to keep reading this post and get 7 days of free access to the full post archives.