Who holds US LNG options, and who cashed them in?

Cheniere, Shell made big — and profitable — changes, while Venture Global made only small cuts

After averaging ~$3.25/MMBtu over the first three weeks of January, winter storm Fern brought sharply more bullish gas fundamentals this weekend. Temperatures dropped 15 or more degrees below seasonal norms across the eastern two-thirds of the country, and forecasts call for this extreme cold weather to last through the week. The first week of February is also forecast to remain colder than normal, albeit less so.

This cold front sent gas demand forecasts and Henry Hub prices skyrocketing. As recently as January 16, the February NYMEX futures contract traded at just $3.16/MMBtu. Monday, it closed at $6.52/MMBtu. The dislocations were even larger in the January market, with Henry Hub cash printing ~$28/MMBtu for the January 24-26 weekend package and balance-of-month trading ~$20/MMBtu.

Gas liquefied this weekend would be sold no sooner than February in destination markets. TTF trades at ~€40/MWh for February delivery, equivalent to ~$14/MMBtu. At ~$28/MMBtu, then, US LNG was ~$14/MMBtu underwater on a variable-cost basis.

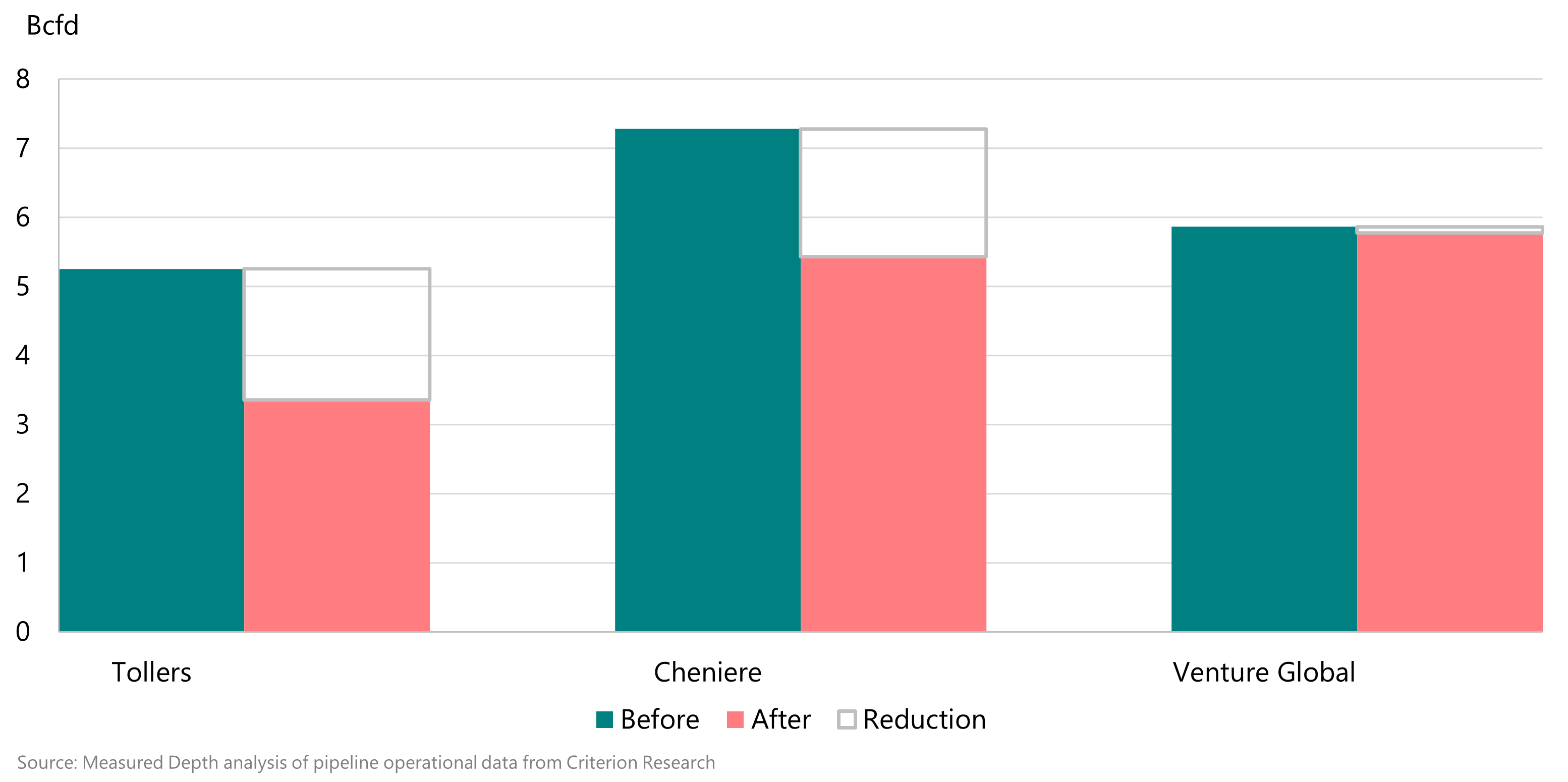

On Saturday — before the storm disrupted Haynesville production and likely precipitated additional involuntary cuts — feedgas reductions totaled ~3.8 Bcfd, with tollers cutting ~36%, Cheniere ~25%, and Venture Global hardly at all. The financial stakes are significant: I estimate Cheniere could have made as much as $80 million by unwinding its feedgas purchases over the weekend.

When Henry Hub price spikes push US LNG this far out of the money, liquefaction is no longer baseload demand but rather a financial option. But who holds that option — and can exercise it for tens of millions — varies by project.

Who holds the options?

In the first wave of US liquefaction, most projects had a commercial structure similar to an interstate gas pipeline, on which a shipper pays a monthly reservation charge in exchange for access to an increment of capacity. The shipper, though, is responsible for buying (or producing) the gas, scheduling the volumes, and then selling (or consuming) the gas. Freeport, Cameron, Elba, and Cove Point liquefaction contracts are structured similarly: the LNG offtaker pays a monthly reservation charge for access to the liquefaction capacity but is responsible for procuring/shipping the feedgas. These LNG offtakers maintain title to the gas through the value chain.

Cheniere’s projects were structured differently, with Cheniere responsible for feedgas sourcing, pipeline and storage contracting, and pipeline scheduling. Cheniere’s counterparties still pay a reservation charge, but at these projects, that is in exchange for the right to receive FOB LNG. Cheniere, instead, has title to the gas until after it is liquefied. Cheniere’s offtakers also pay 115% of the Henry Hub price for volumes they do lift, to cover losses in pipeline transportation and especially liquefaction.

In that first wave, feedgas procurement and transportation were straightforward for companies like BP (at Freeport) or Shell (at Elba), as these firms are among the largest US gas marketers. Other companies, most significantly Toshiba (at Freeport), underestimated the complexity of US gas marketing and ultimately exited US LNG. Not coincidentally, all second- and third-wave US LNG projects use the FOB model pioneered by Cheniere.1

At Cheniere’s facilities, LNG offtakers must exercise their option by the 20th of the month two prior to when they would receive the cargoes.2 That means offtakers made decisions about January cargoes by November 20, when January TTF traded ~$6/MMBtu over Henry Hub.

So while LNG tollers at Elba, Cove Point, Freeport, and Cameron could sell back gas purchases this weekend in response to changing market conditions, the window for Cheniere’s and Venture Global’s customers has long since passed. In the case of Plaquemines, although its final trains came online in December, the project is still pre-commercial, meaning that Venture Global remains the project’s only offtaker.3

But while Calcasieu Pass, Sabine Pass, and Corpus Christi offtakers no longer hold a January (or February) US LNG option, Cheniere and Venture Global themselves still do. Because their customers only take title to the LNG FOB, Cheniere or Venture Global can serve their customers from LNG storage rather than continuing to liquefy gas. They could then cover this short by fulfilling their own DES sales with ~$14/MMBtu LNG from elsewhere or, in a best-case scenario, by refilling LNG storage with ~$6/MMBtu February gas.

Who’s exercising their options?

By analyzing LNG transportation portfolios and pipeline nomination data, I estimate which US LNG option-holders unwound their gas purchases this weekend. This exercise isn’t completely straightforward — some Freeport and Cameron tollers have overlapping feedgas portfolios; some intrastate pipelines serve Corpus Christi and Freeport; Cove Point Pipeline serves other load besides the liquefaction facility — but nonetheless, the results are directionally informative.

In gas markets, the weekend trades on Friday as a Saturday-Sunday-Monday package. Companies can and do make single-day deals, but typically these reflect operational disruptions, such as cuts due to Haynesville production freeze-offs. On Saturday, before Haynesville production declined sharply, LNG feedgas reductions totaled ~3.8 Bcfd, with tollers (in aggregate) and Cheniere cutting much more aggressively than Venture Global. The latter’s reduction came almost entirely at Plaquemines, where it does not yet have customer obligations.

Figure 1 | January 24 feedgas reductions

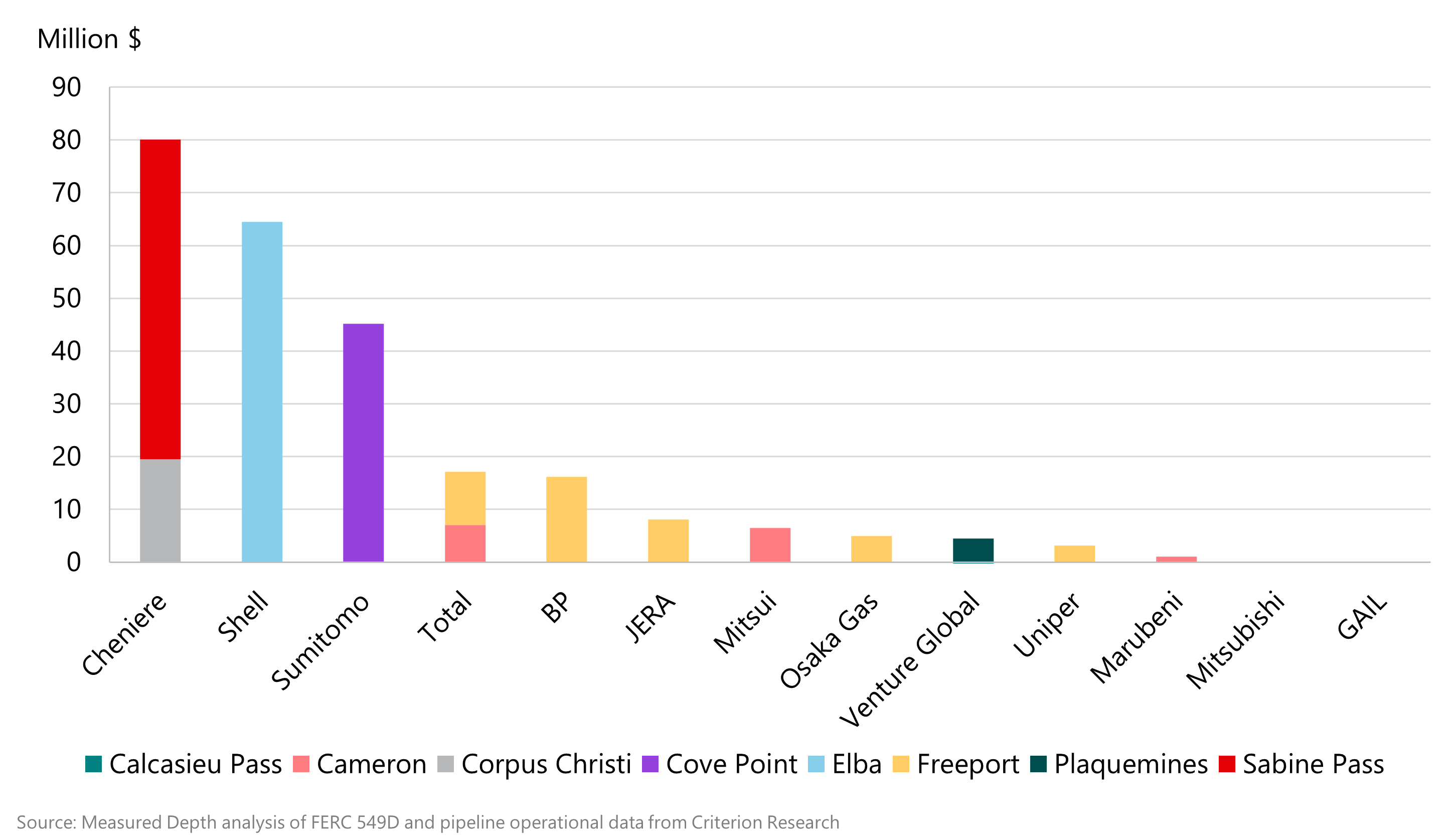

As long as upstream cuts on Sunday and Monday were not significant relative to the total feedgas reduction, the financial impact of Cheniere’s operational changes is likely to be material to the company. In 3Q25, the company reported $1.6 billion in adjusted EBITDA, whereas I estimate that Cheniere could have made as much as $80 million by unwinding its feedgas purchases over the weekend and backfilling these sales with $14 LNG. If the company has sufficient storage flexibility to replace these sold volumes with February (or March) Henry Hub gas at $6 (or $4), the impact would rise to ~$140 (or ~$150) million.

Venture Global, in contrast, made much smaller changes, perhaps due to broader corporate considerations. If the company were to change Plaquemines operations in response to market conditions, it may risk jeopardizing its claim that the facility is pre-commercial. In other words, the value of Henry Hub gas resold this weekend was very high, but nowhere near as high as the aggregate value of all pre-commercial Plaquemines cargoes. Shell and Venture Global have been locked in a lengthy legal dispute about when Calcasieu Pass was commercial, and Shell is also a Plaquemines offtaker.

Among tollers, Shell made the biggest change, reducing Elba feedgas to zero. Despite Elba’s small 2.5 MMtpa size, the change could have been worth as much as ~$65 million to Shell, because Transco Zone 5 traded at more than $60/MMBtu this weekend. At Cameron, feedgas reductions varied by pipeline, with the largest cuts on routes where Total holds the most capacity — though differences in upstream freeze-offs may also explain the pattern.

Figure 2 | Estimated LNG option impact on earnings

How long will this last?

At the four tolling facilities, reduced feedgas is likely to last as long as Henry Hub prices stay higher than those for LNG — at least through the end of the month, based on the latest forecasts. If anything, tollers’ feedgas nominations are likely to continue to decline if prices remain high, as operational factors likely limit how quickly and efficiently a liquefaction plant can ramp down. Inasmuch as US LNG tollers have already on-sold their US cargoes, they could instead procure LNG from elsewhere and pocket the difference between Henry Hub and LNG prices. (Of course, reduced US LNG output is likely to bid up February global gas and LNG prices.)

Cheniere’s ability to maintain FOB LNG deliveries to its customers with lower feedgas intake will dwindle quickly through the week. Most of Cheniere’s customers take LNG FOB, so by week’s end, Cheniere likely will need to renegotiate with them — and surely share the value of its now-deeply-in-the-money option. But with ~$6/MMBtu of value at stake and some of the largest LNG marketers as counterparties, unwinding this option is likely to continue accruing profits for Cheniere.

A third model is underway at Rio Grande and Port Arthur. These projects offer FOB LNG, but NextDecade and Sempra will not manage feedgas and pipeline portfolios. Instead, a major offtaker at the projects — Total at Rio Grande and ConocoPhillips at Port Arthur — will handle domestic gas purchasing for the entire project.

This is also why US LNG exports were high in April 2020 and still low in October 2020

Thank you Amber. In regards to the natural gas in storage, who owns that gas and pays the storage fee? Is it the production company planning to put gas in storage in summer and hopefully selling at higher price in winter or is it utility customer or LNG supplier storing until needed. I realize that this is a basic question, but I am wondering which party was able to take advantage of the price swings in late January. Thank you

The contrast between Cheniere's FOB model and traditional tolling is fascinating—basically Cheniere holds a massive embedded optionality that tollers give up in exchange for feedgas control. Estimating $80M-$150M for one weekend is wild, especially set against quarterly EBITDA. I'd be curious how often these dislocations happen in a typical year vs how much upside they represnt in tail scenarios. Venture Global's hesitation makes sense given the pre-commercial litigation overhang.